The tortuous life of Prop 15 through the Indianapolis-Marion County City-County Council is not the Council's finest hour by any stretch of the imagination.

The ridiculoucity continued this past week with two evenings of meetings of the Metropolitan & Economic Development committee.

Even before Monday night's meeting began, the committee knew it would be recessing that night without passing Prop 15 due to a disagreement with the Ballard administration over a proposed amendment that sought to add language guaranteeing two microloan programs and one job training program. Councillor Vop Osili had a memo from Deron Kintner to the effect that the City agreed to those programs, but wanted it written into the proposal. I uploaded to Google Docs the disputed, and never introduced, amendment. What you'll notice is it's clarity of language. The header suggests this amendment was intended to be voted on at the full Council meeting where, instead, the Council decided to send Prop 15 back to committee.

What was introduced Friday night, after they had four full days and nights to come to an agreement, was a mess - tortuous language construction, dubious protections for the intended beneficiaries of the programs, and massive loopholes. Not to mention the misspelling of the word "Councillor" - which is defined in Council rules, by the way. Plus you'd think commas were an endangered species that had to be included sparingly. This amendment passed by a vote of 6 to 1, with Councillor Zach Adamson providing the sole no vote. I have uploaded my copy of this amendment, as the Council website has not yet updated their version of Prop 15. Sorry for the scribbling, I wasn't thinking I'd be sharing it with everyone.

From the header one might think this amendment would be introduced at the full Council. The meeting Friday night did start 5 minutes late and the amendment was not available until seconds beforehand. So, it may be the negotiations were deemed done enough and this messy amendment was introduced at the committee instead.

Here are some attributes of the amendment that catch my eye:

The $10 million microloan program will require "the leveraging of current resources" which usually means floating bonds to be repaid with some revenue stream. There aren't many details provided on this proposed program. One thing that is stated is that it would be a county wide program. It would be a violation of state law for the funds to come from the downtown TIF.

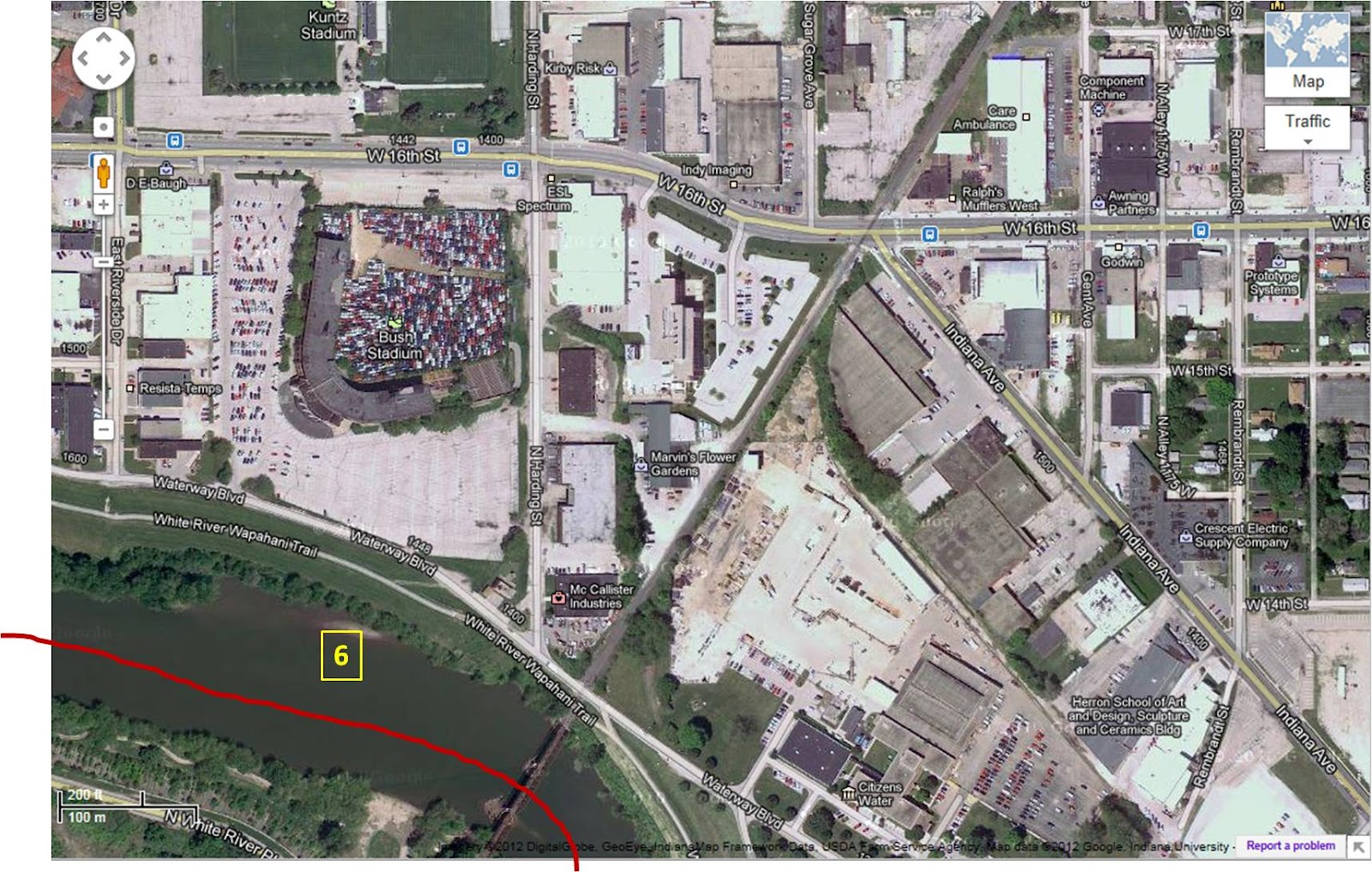

I looked through google street maps and the Marion County Assessor's interactive map to try to locate the "Bryant Heating & Cooling Facility located at 21st and Montcalm". All parcels at that intersection are owned by private entities, none of which are Bryant. To the west, however, at 1100 W. 21st Street, there is a large parcel with large buildings that appear abandoned, which is owned by DMD. Why the lack of specificity when an address or parcel number is three mouse clicks away? This is important because there is an attempt to require the demolition of this facility.

In multiple places the phrase "the area" is used. From context it seems like it refers to possibly different boundaries at times - but the phrase is never clearly defined, which results in little to no protection of the residents of the Bush Stadium area that any of the promises made to them will actually be fulfilled - or even be required to be fulfilled.

The $2 million microloan program can be awarded to any business within a two mile radius of the enlarged downtown consolidated TIF. The language is poor, again a comma or two might clarify, but it is either attempting to say the business must be located in a lower income area (median household income 75% or less of the median income in the County) or that the 2 mile perimeter must be centered on a low income area. Just by the way, the median household income in the County is $40,421. But a two mile radius? How does that adequately target the Riverside or UNWA residents who came out to say they needed help? Looking at maps, this perimeter could reach the Speedway to the west, Garfield Park to the south, Butler University to the north, and nearly Emerson Avenue to the east. The intent is to take the funds from the TIF. But TIF revenues must be spent within the TIF. These requirements are a clear attempt to circumvent the state laws regarding the expenditure of TIF revenues, and it does not target the folks who live in the Bush Stadium area.

The exact same thing can be said of the $1.5 million job training program as was just stated for the $2 million microloan program.

And the last I'll mention is the really botched attempt to get work for the TIF district residents. The language seems to say that any business receiving TIF money, should they require new hiring, would have to ensure that 40% of those hired lived in the TIF district. The business could get out of this by filling out a form that indicated why it tried but failed to get to the 40% figure. Or, they could bring in all their additional help from out of state, since those folks will not be counted.

Osili has been all over town touting the targeted benefits he personally negotiated for the residents and businesses of the Bush Stadium expansion area. But, he is not delivering on that promise with this language. Someone is being scammed - its either Osili or the residents.

Prop 15, that twice beaten dead horse now burdened with the worst amendment in the history of amendments, was voted on twice by the committee Friday night. The first time the phrasing of the motion left off the key part where it would be sent back to the full Council with a do-pass recommendation. On the advice of Council counsel, they did a do-over with the correct motion.

Both times the vote was 6 yeas and 1 nay. Councillor Zach Adamson was the lone no vote both times. The yeas were Councillors Robinson, Talley, Adams, Osili, Miller and Cardwell. The last two are Republicans and the rest are Democrats.

Prop 15, that raggedy, tattered zombie that it is, returns to the full Council Monday night.

Todd Young And The Empty Chair

13 hours ago